Electric Mobility 2.0 — New Mecca for Startups

The Urban Electric Mobility Initiative (UEMI) propagated by UN Habitat has reignited the action in developing electric transportation worldwide. The aim of UEMI is to achieve widespread adoption of electric vehicles in global cities to reach a target where travel by electric vehicles makes up 30% of total urban travel by 2030.

This initiative is likely to contribute in a significant manner:

- Reduction in emissions from transport and limiting the increase in global mean temperature to two degrees Celsius.

- Reduction in local air pollution and improving health

This has given a second wind to the proponents of electric vehicle and can be termed as Electric Mobility 2.0. This development is likely to be highly disruptive for global automotive manufacturers. However, there is a great degree of uncertainty in timing of the inflection point whereby the number of EV manufacturer would surpass IC vehicles. There are several factors which influence the e-Mobility market that needs to be resolved first.

Technology Trends that are transforming automotive industry

The trends are likely to shift market segmentation, change customization paradigm and a new set of pathways for rivalry and cooperation. Technology availability will enlarge to wider base of manufacturers across the globe. The genuine development of EV movement is enshrined in policy frameworks and their implementation, if done well may grow this segment by an average of 40% p.a. globally.

Electrification plays a significant role in a country like India, where we desperately need solutions to reduce the growing levels of pollution in our metropolises. E-Mobility does have a play in pollution abatement but it has to be coupled with charging of batteries using renewable sources of power. Otherwise, it is just shifting pollution from cities to hinterlands. By 2030, e-Mobility 2.0 could prompt electric vehicles (EVs including Battery Electric Vehicles, Plug-in Hybrid Electric Vehicles and Hybrid Electric Vehicles) holding a significant share up to 50% of new vehicle sales in a breakthrough scenario globally. If India experiences the similar momentum, it will significantly impact manufacturers across the automotive value chain.

However, after the initial announcement for adoption of 100% electric vehicles by 2030, India has already rolled back this audacious goal under intense lobbying by automotive component sector.

Concepts of shared mobility are emerging through cab aggregators, use of electric rickshaws and electric buses. However, IoT based inter connectivity and autonomous driving are currently far off concepts on India’s Mobility 2.0 horizon.

Trends in E-Mobility 2.0

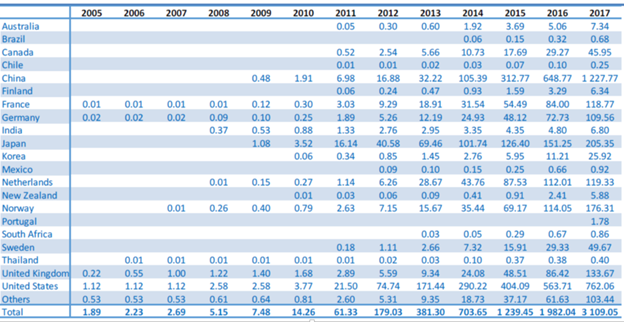

Globally Rising Stock of Electric Vehicles

There were more than 3 million electric passenger cars on the road worldwide in 2017, 40% of which were in People’s Republic of China (“China”).

Among the European countries, Norway has the highest share of electric car with at 6.4% vehicle stock. While the number of electric cars is notably on the rise, only three of the European countries have a stock share of 1% or higher: Norway (6.4%), Netherlands (1.6%) and Sweden (1.0%).

Sales and market shares

In 2017, global sales of electric vehicles crossed the threshold limit of 1 million units (1.1 million). The sales growth of EV was slow in 2016 when compared to 2015 but picked up a pace in 2017, registering a year-on-year increase of 54% (compared with 38% in 2016). China has one of the world’s biggest electric vehicle market and almost 580,000 electric vehicles were sold there in 2017, up 72% from the prior year. China represents half of the worldwide electric vehicle market. Norway is the total pioneer regarding piece of the pie, with 39% of new vehicle deals being electric, an estimate that is six-times higher than Sweden, which has the third-most largest stock of EVs all around (6%), after Iceland (12%).

Electric Mobility 2.0 Defined

Electric Mobility 2.0 is leading to in-vehicle commuting assistance for EV mobility, enabling more reliable and energy-efficient electric-mobility. To have higher impact, Electric Mobility 2.0 adopts a strategic paradigm to address the main concern of urban EV mobility, i.e, Range anxiety. This fact relates to the limited EV range, shortage of parking spots with open charging stations and congestion of urban streets. It seeks to utilize co-operative interconnected systems utilizing IoT technology to simultaneously remove these bottlenecks as a goal. Such an improvement if accomplished will ensure quicker adoption of both private and public electric transportation for EV owners.

Key Drivers for Electric Mobility 2.0

As has been discussed in many forums that government regulations and incentive structures for EV ownership has a major impact on their adoption. The technology which is evolving and seeking to remove many irritants of current generation of electric vehicles is also going to play a great role in faster growth of this market.

The infrastructure such as charging, battery swapping, inductive roads and IoT connected parking slots for EVs is the next set of growth driver for this industry.

With addressal of some of the above and growing environmental concern among the millennial is definitely going to give a fillip to customer demand.

All of the above drivers of e-mobility 2.0 create definite spaces or niches for entrepreneurs to cash on and develop new business models.

Demise of E-Mobility 1.0

Electric vehicles are not a new phenomenon, as they first appeared in the mid-19th century. In fact, an electric vehicle held the vehicular land speed record until around 1900. Interest in electric motor vehicles had greatly increased in the late 1890s and early 1900s. As a matter of fact, electric vehicles of those days had a number of advantages, as they did not have the vibration, smell, and noise associated with over their early-1900s IC car competitors. Further, they also did not require gear changes. These cars were also preferred because they did not require a manual cranking effort to start unlike their gasoline brethren cars. Sales of electric cars peaked in the early 1910s.

However, the high cost, low top speed, and short range of battery electric vehicles, compared to later internal combustion engine vehicles, led to a worldwide decline in their use; although electric vehicles have continued to be used in the form of electric trains and other niche uses.

After years outside the limelight, there was a renaissance of sorts brought by the energy crises of the 1970s and 1980s, due to the perception that electric cars are insulated from the fluctuations of the hydrocarbon energy market.

Throughout the 1990s, interest in electric cars again waned as customer preferences shifted to big bulky SUVs which were gas guzzlers, though affordable to operate, thanks to lower gasoline prices.

It was only with the emergence of TESLA in 2004, and introduction of their earlier models in 2008, brought EVs back into mainstream.

Transition from E-Mobility 1.0 to 2.0

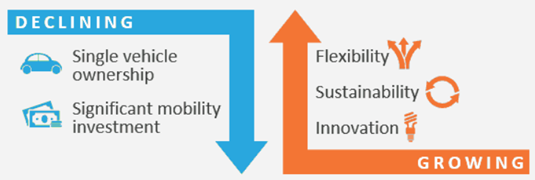

There are many reasons for transition from the hither to dead e-mobility 1.0 to e-mobility 2.0. One set of reasons are encapsulated in the graphic below.

The consumer preferences, especially of the emerging millennial generations are changing. They strongly believe in concepts of shared economy and significantly conscious of sustainable development. They embrace innovation far quickly, are highly flexible and ready to experiment with emerging technologies as long as it meets their perceptions.

The second set of reasons are presented in graphic below.

The shifting sands of technology are disrupting the whole terra firma of automotive landscape. The days are not far which will lead to emergence of non-fossil fuels autonomous cars operating on business models of shared economy. This would be the true emergence of E-Mobility 2.0.

Possible Opportunities for the Startups in the era of E-Mobility 2.0.

1. Electric vehicle Manufacturing

Innovation lies in manufacturing of electric vehicles across the spectrum of high-end sports cars to urban commuting cars to public transportation vehicles such as e-Rickshaws. There are sweet spots for technology augmentation and cost reduction.

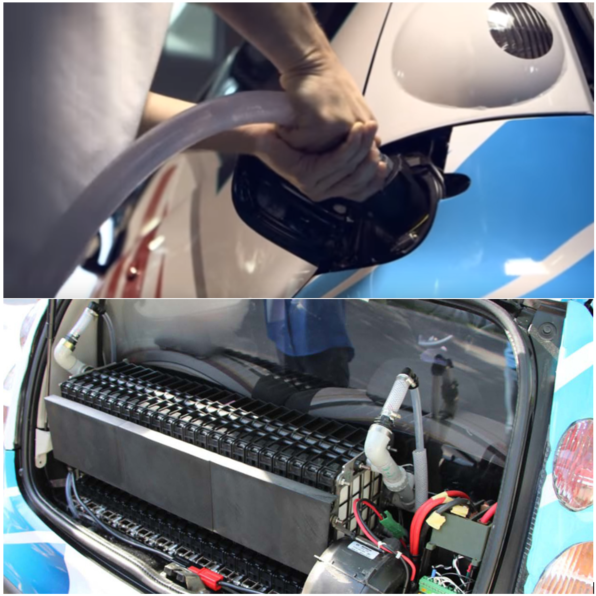

2. EV charging Infrastructure

Adoption of EV walks hand in hand with its charging infrastructure. It is a crucial element of EV infrastructure that supplies energy for recharging of EVs such as plug-in electric vehicles, including electric cars, neighborhood electric vehicles and plug-in hybrids. Many interesting business models are emerging in this space for entrepreneurs to latch on.

3. Lithium-ion battery manufacturing

Most electric vehicles use lithium ion batteries. Lithium ion batteries have higher energy density, longer life span and higher power density than most other practical batteries. The huge penetration of EV in market will increase the need for batteries which either import or manufacture locally. There are interesting ideas around smart batteries, standardized batteries to support concepts of battery swapping and Geo-locating any battery worldwide.

4. EV motor manufacturing

Being the work horse of EV, it provides propulsion and mobility to vehicle. There are many interesting research ideas and manufacturing innovations around motors to make them more powerful yet lighter. These ideas could lead to spinning of startups.

5. Internet of Things

The Internet of Things (IoT) technologies are fast emerging with their applications in interconnecting network of physical devices, vehicles, charge points, parking slots, and other items of e-mobility 2.0 ecosystem. New generation EVs, embedded with electronics, software, sensors, actuators, and connectivity which enables these things to connect and exchange data. The emergence of such technologies give interesting niches for entrepreneurs to innovate and create new business models.

Characteristics of EV Startups team

- Strong Management team for EV startup is critical for successful commercialization

- Requires multidisciplinary competencies (from mechatronic engineering to computer sciences)

- Should be savvy in emerging EV policy frameworks

- Managing required network, industry and government

Case studies for start-ups in E-Mobility 2.0

BlockCharge

BlockCharge is a working prototype for Electric Vehicle Charging on the Ethereum BlockChain. Electric Vehicles or their owners authenticate themselves via a Smart Contract at the charging pole. The charging pole switches turns on the power and starts the charging process. Billing is done automatically via the use of cryptocurrencies. The Blockchain offers an affordable and seamless way to establish a global charging infrastructure.

Users install an app on their smartphones to authorize the charging process. It connects to blockchain, which manages and records all of the charging data. The app automatically negotiates the best price and manages the payment process automatically. BlockCharge’s business model is based on the one-time purchase of a Smart Plug and a micro-transaction fee for the charging process.

Phinergy

Phinergy is an Israeli startup founded in 2008 which has developed high energy density systems based on metal-air energy technologies. Phinergy’s aluminium-air technology enables to store, transport and discharge clean energy around the world. Phinergy’s aluminium-air systems produce energy by combining aluminium, oxygen, and water. Oxygen is a key reactant releasing energy from metal. Unlike conventional batteries that carry oxygen within a heavy electrode, metal-air energy systems freely breathe oxygen from ambient air, making the systems significantly lighter.

It offers aluminum-air and zinc-air batteries for transportation, stationary energy storage, aerospace and defense, consumer electronics, and chlorine production applications. They have demonstrated a range of 1600 k.m by using aluminium air battery, however water has to be replenished every 200 k.m.

EV Safe Charge

Los Angeles-based EV Safe Charge isn’t focused on next-gen electric vehicles, but rather the infrastructure that will support them. Similar to Solar City’s solar panel distribution, EV Safe Charge is aiming to become a one-stop shop for the installation of electric vehicle charging stations for all levels of customers from residential to commercial. The company offers a variety of chargers from suppliers including Bosch, ClipperCreek, EV-Box, EV Connect, and JuiceBox.

Ather Energy

Ather is the largest startup operating in e-mobility space in India. It is founded by IIT graduates Tarun Mehta & Swapnil Jain in 2013 and is among the few EV hardware start-ups in India. The company is looking to produce a range of premium smart two-wheelers targeting the high-income Indian users.

Ather came into the limelight when it raised INR 180 Crore from Hero Motocorp in a funding round which concluded sometime ago. The company had, previously, been backed by venture capitalist firm Tiger Global and Flipkart founders, Sachin and Binny Bansal.

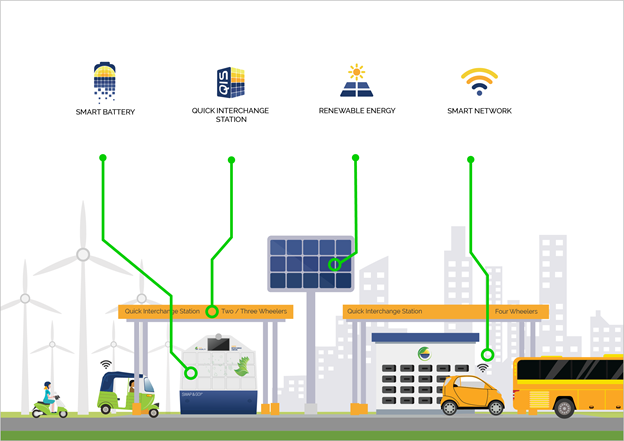

Sunmobility

Sunmobility has been founded by Chetan Maini, the poster boy of e-mobility in India. This company aims to build customized solutions for India’s changing mobility needs.

The challenges in India’s urban transportation are unique and require a tailor-made solution. As specialists in the field of electric mobility and renewable energy it has created an open-architecture, ‘Smart Mobility’ model deployable across multiple vehicle platforms — 2 and 3 wheelers, cars and buses. This “Made in India” solution tackles four main roadblocks in mass EV adoption like high costs, long charging time, equivalent infrastructure, and range anxiety.

Conclusion

The electric mobility industry can not only give an impetus to economic development but also contribute to reduction of carbon footprint. Considering the entire value chain of e-mobility including renewable energy generation and distribution, recharging, battery and components, and Electric Vehicles sales, a World Bank study indicates a total value chain greater than $250 billion worldwide.

The gains of e-mobility can only be accomplished with improvements in urban planning and design and a focus on “people centered planning”. For e-mobility to become a reality, greater emphasis should be given to develop adequate streets and public spaces in cities. This has to be accompanied by improvements in public transport and integration between public and non-motorized transport.

To achieve the potential of E-Mobility in mitigation of GHG emissions, a shift to cleaner and renewable sources of energy and more efficient energy transmission and distribution will also be required. If this is done, then E- Mobility can play a vital role beyond the MDG development framework. Question remains how to inspire the next generation of business leaders to adopt even more ambitious sustainability goals and of course how do we give Mobility innovators and entrepreneurs the best chance of success.

About the Author: Dr Parag Diwan is a noted energy professional and founder of EV Oracle, a niche consulting firm in e-mobility. <www.evoracle.com> He has built many fine institutions including the largest Energy University in India